Payment processing feels simple on the surface. A customer taps a card. You get paid.

Behind the scenes, however, multiple banks, networks, risk systems, and pricing layers determine how quickly you get funded and how much you actually keep.

If you run a business in Canada, understanding this system is not optional. It directly impacts your margins, cash flow, and risk exposure.

This guide explains how payment processing works, what fees actually mean, and where merchants typically overpay.

What Happens When a Customer Taps a Card?

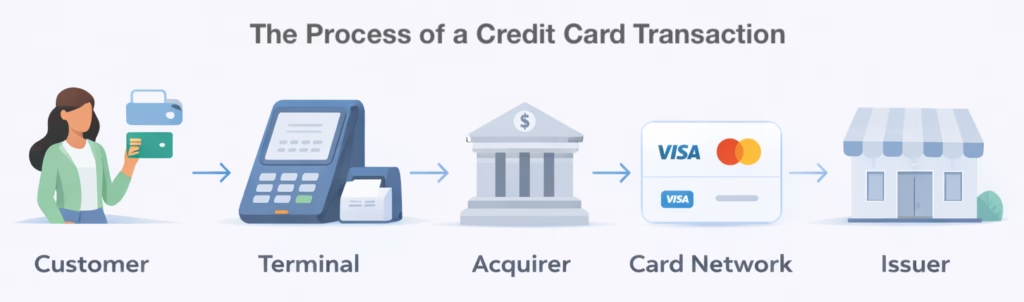

When a customer taps, inserts, or enters their card, the transaction feels instant. Behind the scenes, however, several institutions communicate in milliseconds to approve the payment and move funds.

Here’s what actually happens:

1. Customer Initiates the Payment

The cardholder taps, inserts, or enters their card details. The terminal encrypts the transaction data and sends it for authorization.

2. Terminal Sends the Request to the Acquirer

Your payment processor, also called the acquiring bank, receives the transaction and routes it through the appropriate card network.

3. Card Network Routes the Transaction

Visa or Mastercard forwards the authorization request to the customer’s issuing bank.

4. Issuing Bank Approves or Declines

The issuing bank checks available funds, fraud signals, and risk factors. It then sends an approval or decline response back through the network.

5. Approval Flows Back to You

The response travels back through the card network and acquirer to your terminal. If approved, the transaction is completed and funds are queued for settlement.

What Happens Next?

At the end of the business day, transactions are batched and submitted for settlement. Funds are typically deposited into your account within 1–3 business days, depending on your agreement and risk profile.

The 3 Core Fees Merchants Pay

Every credit card transaction is made up of three separate components, even if your statement shows only one blended rate.

The first is interchange, which is paid to the cardholder’s issuing bank. It varies based on card type, rewards level, debit versus credit, and whether the transaction is in-person or online. Interchange is set by the card networks and cannot be negotiated.

The second is network assessment fees, which are paid to Visa or Mastercard for using their payment rails. These are standardized and typically small relative to the total transaction cost.

The third is processor markup. This is the portion retained by your payment processor for providing technology, support, risk management, and profit. It is the only component that a processor directly controls.

Pricing Models Explained

Not all payment processors price the same way.

Two merchants processing the same volume can pay materially different effective rates depending on how their agreement is structured. In Canada, most processors use one of three models: Tiered Pricing, Flat Rate Pricing, or Interchange Plus.

| Model | Transparency | Cost Efficiency | Best For |

|---|---|---|---|

| Tiered | Low | Variable | Only for advanced merchants |

| Flat Rate | Medium | Lower at small volume | Micro businesses |

| Interchange+ | High | Best at scale | Growth-focused merchants |

Tiered pricing groups transactions into categories such as qualified and non-qualified. It is simple to present but often lacks transparency. Merchants typically cannot see how transactions are classified, which makes the true cost difficult to audit.

Flat rate pricing applies the same percentage to every transaction regardless of card type. It is predictable and easy to understand, but it often becomes expensive as volume increases. Lower-cost debit transactions can end up subsidizing higher-cost premium credit cards.

Interchange Plus separates the underlying interchange cost from the processor’s markup. This structure makes it clear what portion of the fee goes to the issuing bank and what portion goes to the processor. For growing businesses, it is generally the most transparent and economically efficient model.

The pricing model matters more than the headline rate. The only component a processor controls is their markup. Everything else is set by the card networks.

What Impacts Your Effective Rate?

- Rewards and corporate cards cost more

- Debit vs credit ratio

- Industry risk level

- Average transaction size

- Monthly processing volume

- Chargeback history

- Card-present vs online mix

Not Sure What You’re Paying?

Most Canadian merchants don’t know their true effective vate. We will review your statement and well break it down clearly.

Red Flags to Watch For in Payments

- Long-term contracts with automatic renewals

- Early termination fees that are hard to quantify

- Equipment leases that outlast the hardware

- Bundled pricing with no interchange breakdown

- “Free” terminals tied to multi-year agreements

- PCI compliance fees that are unclear or recurring

- Statement formats that make auditing difficult

- Sudden rate increases without clear explanation

Should You Switch Payment Processors?

If your pricing is transparent, your contract flexible, and your support responsive, you may not need to.

But if you don’t fully understand your fees, are locked into long-term contracts, or cannot access real reporting, it may be time to reassess.

Understanding the system is the first step. Improving it is the next.